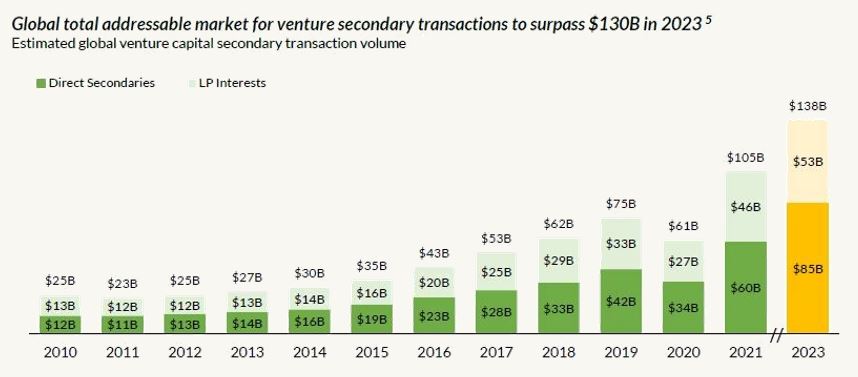

How Big Is the Secondary Market for Venture Capital? An Updated View to a $130B Market

In Q3 2019, Industry Ventures published “How Big is the Secondary Market for Venture Capital?”, which detailed our estimate of the size of the US secondary market for venture capital as well as a discussion around the driving forces behind the market’s growth. Since the US now only accounts for less than half of the global venture capital market, we’ve broadened this report to include the international market as well. We believe the global total addressable market for venture secondary transactions reached $100 billion in 2021 and is on track to exceed $130 billion in 2023.1,2 Internally, we continue to see both seller supply and transaction volumes grow and believe the market is still underpenetrated by almost any measure.

Despite increased attention, the venture secondary market remains difficult to size compared to other financial markets; secondary transactions occur in many forms including share transfers, LP transfers and fund recapitalizations, continuation funds, etc., and none of these are consistently reported or publicized. Different reports use different methodologies, which result in a wide range of estimates. Having operated as one of the leaders in the venture secondary market for over 20 years, we’ve watched this market evolve first-hand as different investment structures developed, different seller types began seeking liquidity and various sources of supply emerged. Leveraging publicly disclosed data, along with our proprietary internal information, we believe the venture secondary market will grow to over $130 billion in 2023. This is being driven by several tailwinds, including growing allocations to venture capital, extended time horizons for startup exits, increased investor demand for liquidity and the proliferation of new secondary deal structures, resulting in a large and expanding venture secondary market.

A Steady Supply of Sellers to Drive the Market

The basis of our estimate is predicated on the steadily growing supply of sellers in the market, coming primarily from the following three sources:

- Preferred and Common Stock in private companies grew dramatically over the last three years – a steady supply of founders, employees and venture funds that hold direct shares in companies (typically 1-3 percent of the direct venture capital market transact in secondary market)

- Limited Partnership Interests and new venture capital funds dramatically increased over the last three years – a growing supply of limited partnership interests in venture funds (including from corporate venture capital groups, hedge funds and other nontraditional investors), which we expect will account for an increased proportion of secondary deals in the future

- GP-led transactions – whether pressured by LPs for liquidity or to extend the life of older funds, venture capital GPs have increasingly embraced the secondary market as an alternative path to liquidity and exit. This increased activity should lead to a trend toward larger deals in the market.

When trying to grasp the breadth of the venture secondary market, it is important to note that both direct shareholder positions and limited partnership holdings (which indirectly hold shares) can transfer, independently. In most cases, these parties are not aware of each other’s secondary market transactions. This effectively doubles the addressable size of the secondary market relative to the underlying value of venture capital assets.

Investors Grew Their Commitments to Venture Capital Dramatically

Since the inception of Industry Ventures in 2000, the venture capital asset class has grown over 10x in size. Institutional and high net worth investors continue to grow their commitments to venture capital in search of alpha and to gain exposure to the fast-growing technology sector. As a result, traditional venture capital firms raised over $1.7 trillion over the last 10 years, compared to just $406 million over the prior 10 years. We have also tracked an exponential increase in the number of venture capital funds being formed each year. From 2016-2021, a whopping 12,600 new venture funds came into existence. This was more than 2x the 6,100 funds formed across the prior six years, which was again more than 2x the 2,700 funds formed across the prior six years.1

The growth of the primary venture capital market is fueling the secondary market with supply of sellers and investments.

GP-Led Transactions Emerge in Venture

In private equity, GP-led transactions have been a popular way to extend a fund’s life, have GPs hold on to their best companies beyond the typical ten-year term and to restructure older funds. While Industry Ventures has been doing GP-led restructurings since the early 2000s, these deals have only recently gained popularity across the broader venture community. Some may recall New Enterprise Associates’ $1 billion+ secondary sale in 2019, which marked the largest publicly disclosed venture fund restructuring ever. In some ways this transaction signified the venture community’s embracement of these deals.

These transactions allow GPs to generate either full or partial liquidity by restructuring their LP base to extend their funds beyond the 10-year term life or by strip selling certain value-driving assets, and with prominent venture groups leading the way, we expect to see a growing prevalence of these deals in the coming years. This should also result in a trend towards larger secondary market deals over time, as GP-led deals are entire or partial fund positions vs. smaller one-off shareholder or single LP positions.

Startups Continue to Remain Private for Longer

As investors continue to flow into venture capital, the availability of growth capital has allowed companies to remain private for longer, focus on growth and put off IPO prospects until significant scale has been reached.

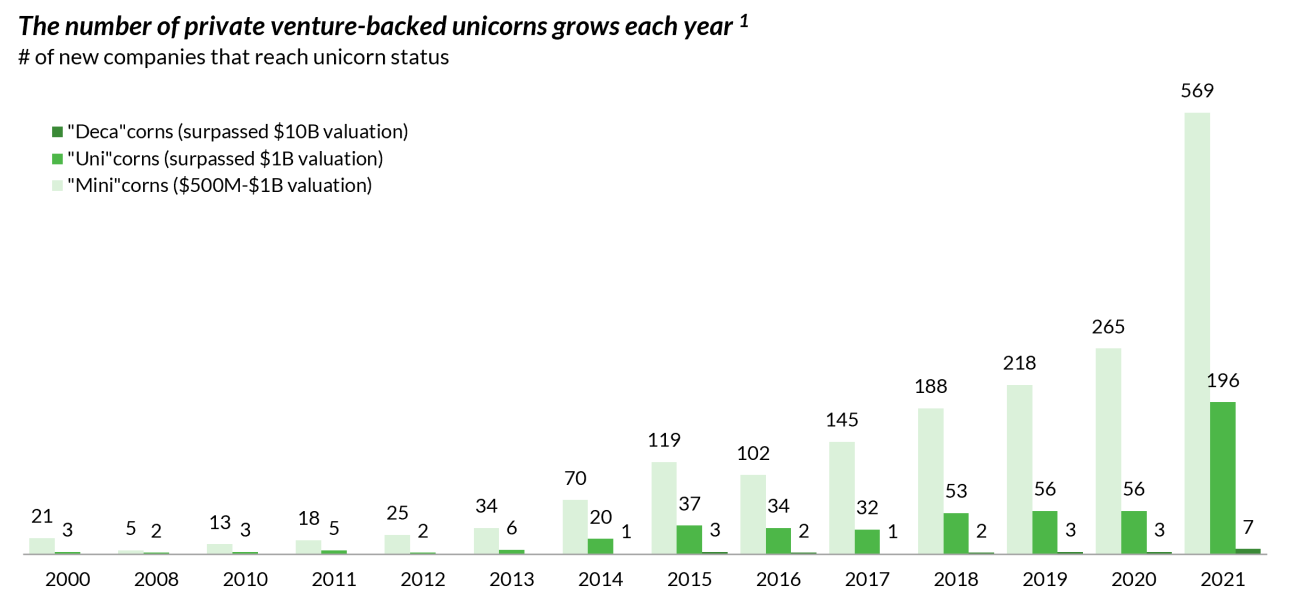

In 2021, the average company that went public was 12 years old and generated $200 million in annual revenue, compared to only 6 years old and $30 million in revenue in 1989.3 Even accounting for inflation, this still represents a 3x increase in the annual revenue base.

Companies are waiting to grow 3-6x larger than their predecessors before going public, thus the backlog of venture-backed unicorns has grown dramatically. While there were fewer than 15 venture-backed unicorns in existence back in 2012, there are currently over 1,300, collectively representing over $4.6 trillion in post-money valuation.4 Unfortunately, the traditional paths to exit are relatively narrow. Even in 2021, which was the hottest IPO and M&A year ever recorded, only 209 unicorns went public or were acquired.1

As the time horizon for companies to exit continues to extend, this will only grow the existing backlog of unicorn companies over the following years.

Value Accumulation in Unicorns Drives Demand for Liquidity

As the time to IPO extends past an entire decade, shareholders of venture-backed companies are forced to wait longer and longer to realize their gains, with each new round of funding implying another 1-3 years of waiting.

This can be an issue for LPs of venture funds who invest against 10-year time horizons. Often these LPs find themselves in funds well beyond the original term life, concentrated in a couple of unicorn assets that are still years away from going public. Over the years, we’ve tracked a growing volume of LP interest deal flow with this exact issue. In fact, ~40 percent of the deals we closed in Industry Ventures Secondary Fund VIII were LP interest deals, up from only ~20 percent in Fund VI.

In total, we estimate there to be $1.1 trillion of unrealized net asset value (NAV) currently remaining in venture funds that are 2016 vintage year and older.1,2 This represents a large and growing supply of possible LP sellers over the coming years.

Alternative Capital Sources Also Drive Secondary Supply

We’ve also tracked exponential growth in activity by crossover funds, hedge funds, family offices, sovereign wealth funds, asset managers, corporate venture groups, and universities as well as other “nontraditional” venture investors. While many of these groups are highly sophisticated and have built solid reputations as Tier 1 venture capital investors, the unprecedented ramp-up of both funds and deployment activity over the last decade implies the prevalence of latecomers.

Even in healthy bull markets, there is a regular and natural churn of both traditional venture capital firms and nontraditional investors out of the market. Historically, however, we have noticed that the churn of nontraditional funds elevates in extended bear markets. These groups have entered and exited the market in a highly cyclical pattern, often utilizing the venture secondary market to divest their interests. Therefore, if current market conditions persist, we can expect some of the recent latecomer funds to become suppliers in the secondary market.

In conclusion, there are a number of underlying tailwinds that we believe will push the venture secondary market past $130 billion by 2023. The market is large, expanding, often undercounted and underpenetrated by almost all measures. Companies are staying private for longer, and in response LPs and GPs have fully embraced the secondary markets as a practical third option to liquidity where they are able to control the timing of their exit, unlike in a traditional IPO or M&A. While the current market environment has caused deal activity across most asset classes to slow, we believe deals in the venture capital secondary market are poised to accelerate over the coming years.

Endnote: Defining Venture Capital Secondaries

Although there is no singular definition of what constitutes the venture capital secondary market, we define it as “transactions involving previously purchased investments, or assets, where the underlying value is in the form of equity value of a privately held venture-backed company (not to include M&A or publicly traded company related transactions)”. The most common investment examples we see include:

- Common and Preferred Stock – Founders, employees and venture funds that sell their shares in private venture-backed companies (also known as “secondary directs”)

- Limited Partnership Interests in Venture Capital Funds – LPs that sell their fund commitments to a third party (also known as “LP interest secondaries”)

- Limited Partnership Interests or LLC Interests in Continuation Funds or Recapitalized Venture Funds – these transactions involve both the General Partners of a venture fund and the Limited Partners. Some of these investments involve extending a fund-life beyond its stipulated term (also known as “GP-led secondaries”)

- Derivative and Structured Loan Securities – to a lesser extent special situations which may include swaps, collateralized loans, forward contracts and preferred equity financings (also known as “special situation secondaries”). Preferred equity financings have been growing in popularity recently, a structure in which the buyer purchases preferred equity rights with interest in the seller’s portfolio/assets, allowing the seller to retain ownership and upside potential.