Private Equity Appetite for Venture Buyouts: A Look at Value Creation Post-VC

Introduction

Four years ago, Industry Ventures examined a trend of VC-backed companies increasingly exiting to buyouts (White Paper: Small Tech Buyout – The Fourth Exit Option) – which ultimately led Industry Ventures to launch its hybrid Tech Buyout Fund strategy focused on the small cap buyout ecosystem. Since then, we have seen the number of venture-backed companies exiting to private equity buyout funds, in both absolute and relative terms, continue to scale. This trend has largely been driven by record levels of dry powder within the PE/VC ecosystems and lower overhead costs associated with establishing and maintaining software-focused companies.1 While many focus on the headline-grabbing unicorn and decacorn venture outcomes, the vast majority (88%) of venture-backed companies that exited over 2017-2021 did so at exit enterprise values of less than $500M.2 In our opinion, the capital-efficiency of SaaS business models continues to attract private equity buyers to hundreds of venture-backed businesses, with private equity being increasingly viewed as a stable exit alternative to the volatile public markets for VC-backed companies.

In today’s environment, with technology valuations compressing and the IPO window closed, venture-backed companies are re-evaluating their capital needs and prioritizing profitability over growth, which we believe will further catalyze these companies to contemplate a buyout exit. We believe that private equity’s appetite for technology, especially software, will remain strong, driven by a large supply of VC-backed companies and buyout’s abundance of dry powder, coupled with powerful secular tailwinds as enterprises lean on technology for productivity gains against inflationary pressure.

But what typically happens to the venture-backed company after it transitions to private equity ownership? We will attempt to shed some light on venture buyout activity and how buyout managers are further capturing value post-close.

Venture Buyouts: A Refresher

Activity Recap

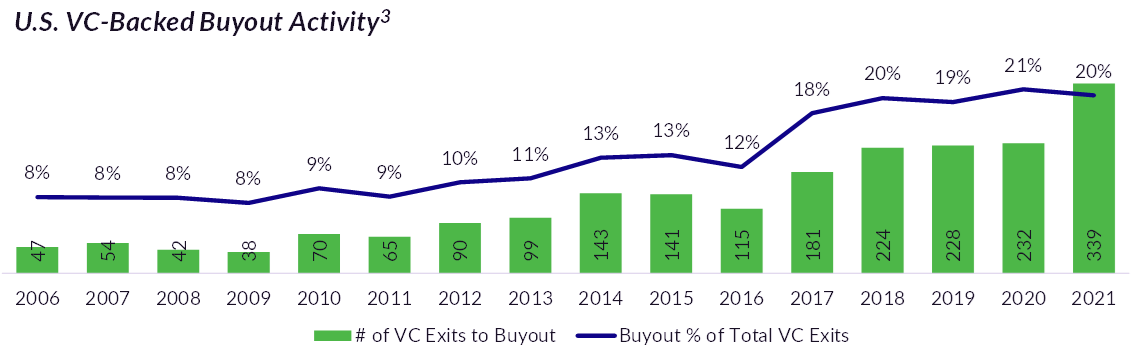

In absolute terms, U.S. VC-backed buyouts grew 46% YoY in 2021 while also consistently accounting for ~20% of total VC exit activity during each of the past five years.3 This increase in transaction activity is driven by several key dynamics, including the growing number of SaaS-based companies that are venture-backed, the large opportunity set created by VC-backed companies staying private longer, and the significant dry powder in the buyout ecosystem. We expect these forces to continue to drive venture buyout activity going forward. In addition, we believe that the recent market environment will further drive venture buyout activity as VC-backed companies become mindful of their cash runway and prioritize profitability over growth.

As illustrated in the graph below, private equity appetite for venture-backed companies has grown steadily: since 2017, the average venture buyout deal size has generally been higher than (or in line with) the average deal size associated with strategic acquisitions of venture-backed companies.6

It should come as no surprise that a majority of the targets for these venture buyouts have been tech companies, with the sector representing 56% of venture buyouts since 2019 and healthcare and B2B services representing 16% and 15%, respectively.7

Furthermore, about 58% of the 886 venture buyouts that have been completed since 2019 were add-ons to sponsor-backed platforms and about 42%, or 374, were new platform investments.7 This is consistent with buyout funds utilizing buy-and-build strategies to enhance product offerings, deepen and/or expand customer bases, acquire key talent, and scale companies efficiently.

Some PE funds have been more active in purchasing venture-backed companies than others. The list of the 30 most active venture buyout PE funds includes many technology specialists such as Vista Equity Partners, Insight Partners, Thoma Bravo, Francisco Partners, Silver Lake, and Accel-KKR, illustrating that technology investors are some of the most active in venture buyouts. In addition to these larger funds that are active in acquiring add-ons, many smaller tech-focused buyout funds have also taken notice and are active in venture buyouts as sources of both add-ons and attractive new platform investments.

Profile of a Venture Buyout

In our view, the prime candidates for venture buyouts tend to be software and tech-enabled services companies with a combination of steady ARR growth, capital efficiency (i.e. breakeven cash flows or a clear path to near-term profitability), and defensible customer retention. These attributes provide a basis for the kind of risk-return profile that buyout GPs ultimately seek to underwrite.

Growth Beyond the Venture Buyout

PE investors have a variety of tools at their disposal to drive value creation over the course of their investment period, but the main “levers” we often see pulled within the context of venture buyouts are (i) operational improvements, (ii) accretive M&A, and/or (iii) multiple expansion on exit.

Operational Improvements

The functional areas that we often see buyout investors lean on to drive future scale and growth are sales, product, and finance. Many stand-alone platform transactions we see are subscale or have had limited growth-oriented investment in the past several years. Buyout investors see this as opportunity to create a repeatable go-to-market motion, scale the sales team, improve back-office infrastructure and reporting systems to develop trackable KPIs, and, in select instances, add to or augment the management team. Each value creation plan is tailored to a given company’s specific strengths and identifiable areas for development. For example, sales initiatives can range from accelerating key hires to a full refresh of a company’s go-to-market strategy. Based on our internal data set, within one year of PE ownership, previously venture-backed companies were able to accelerate top-line YoY growth on average from 19% to 25% and drive to positive EBITDA margins, where in many cases, the businesses in question were not profitable when acquired.8 These statistics highlight how private equity owners are able to repeatedly boost growth and profitability, and we expect these metrics to become even more pronounced with time.

Accretive M&A

Many venture buyouts can serve as platforms for future add-ons or be themselves an add-on for a larger sponsor-backed strategic acquiror. Of the 886 venture buyouts that were completed between 2019 and April 2022, 42% were platform investments, and 63% of those platform investments went on to complete at least one subsequent add-on (with an average of ~2 add-ons per acquisitive platform).9 To date, across our Tech Buyout portfolio, over 35% of our 50+ companies have completed at least one add-on. This is in line with market trends, as add-on activity accounted for 71% of all buyout activity from 2019 through March 31, 2022.10

A buy-and-build approach, if executed well, can help transform a subscale business into a mature contender with a broader and/or deeper product portfolio, enhanced talent, wider geographic footprint, complementary customer sets, and stronger go-to-market capabilities.

Multiple Expansion

As VC buyout targets gain scale through organic and acquired growth, their business and financial profiles become more attractive to strategic buyers and larger financial sponsors, often leading to a re-rating of the companies’ valuation multiples. Our internal proprietary data set showed that the average EV/LTM revenue multiple over the prior six years for VC buyouts was 6.1x.11 This represents a substantial discount to the median Q1 2022 EV/LTM revenue multiple for public SaaS companies of 9.8x.12 Increasingly, the buyer in such a transaction is another PE fund (a sponsor-to-sponsor transaction); such transactions accounted for approximately 52% of all PE exits from 2019 to March 31, 2022.13 In Q1 2022 alone, sponsor-to-sponsor transactions accounted for 56% of all PE exits, the highest percentage on record, as other exit pathways became inaccessible.13

What’s Next? Looking Ahead for Venture Buyouts

Per data from Preqin, there is more than $85B of unrealized value in venture fund vintages past the 10-year fund term.14 This combination of unrealized value and term life will push venture managers to find buyers for their portfolio companies, enabling the growth of venture buyouts.

Given the recent pivot of public market valuations and the increasingly uncertain macroeconomic environment, we expect investors to re-evaluate their portfolio construction needs and capital allocation in relation to venture funding rounds. With less funding available, we believe that venture-backed businesses will focus on cash management and prioritize profitability over growth.

In addition, with a muted tech IPO market (which year-to-date April 19, 2022 saw eight tech firms listed on U.S. exchanges vs. 33 in the same period in 2021)15, more companies and their investors may view strategic and/or buyout exits as being increasingly viable and attractive.

This combination of unrealized value, fund term life considerations, a challenged IPO market, and a shifting of company priorities will push venture managers to find alternative exit pathways for their portfolio companies, furthering the growth of venture buyouts, with many buyout managers waiting in the wings.