INTRODUCTION

To better understand the impact of COVID-19 and its related government mandates on the venture capital industry, we surveyed our universe of venture funds. Nearly all respondents were VC fund CFOs or General Partners.

The goal of this survey was to gauge the venture capital-related economic impact of COVID-19 and its associated government regulations, and how the consequent actions of industry stakeholders are affecting the VC space. The data that we collected suggests that these various elements are driving the following trends in our industry:

- Negative valuation impacts

- Portfolio company headcount reductions

- Moderated investment pace

- Extended fundraising timelines for VCs

TODAY’S ENVIRONMENT: VCs OVERWHELMINGLY AGREE THAT WE’RE ENTERING A RECESSION

86% of respondents believe that we are entering a recessionary period.

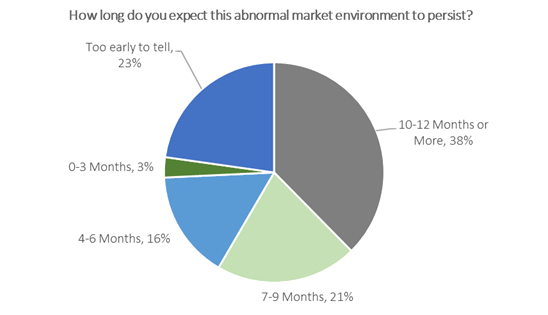

MOST VCs BELIEVE “ABNORMAL” CONDITIONS WILL CONTINUE FOR AT LEAST SIX MONTHS

While 19% of those surveyed expect a recovery within six months, the majority —59%— believe that it will take at least 7 to 12 months to return to a more normalized environment.

VENTURE CAPITALISTS ARE PREDICTING NEGATIVE VALUATION IMPACTS FOR THE DURATION OF 2020

More than half of respondents expect the coronavirus pandemic to have a moderately negative impact on venture valuations, though just over a quarter say it’s too early to tell. Only 6% do not expect to see any impact on portfolio values.

NEARLY ALL VCs SEE PORTFOLIO COMPANY HEADCOUNT REDUCTIONS

Only 8% of those polled do not expect any headcount changes in their portfolio companies. Nearly all venture funds are seeing headcount reductions (92%), with the majority of our respondents signaling 11-30% cuts.

VCs SAY THEIR PORTFOLIO COMPANIES ARE, ON AVERAGE, WELL-FINANCED

The vast majority of survey participants—93%—reported that their portfolio companies have at least 7 months of cash on hand to fund their operations, while just over half expect to have 13-24 months of runway.

IMPACT ON VC INVESTMENT PACE & LIMITED PARTNERSHIP DYNAMICS

Interestingly, venture fund Limited Partners do not appear to be signaling to GPs that they would like to see a slower investment pace during this period of uncertainty and volatility. Only 16% of our survey respondents have received feedback from Limited Partners asking them to slow capital deployment.

Regardless, most venture funds do plan to slow their investment pace, with 30% of managers anticipating a dramatic decrease of more than 25% in the 2nd quarter and 27% slowing deployment moderately (between 0-25%).

Despite the current uncertainty, most funds do not yet anticipate COVID-19-related secondary transfers. However, 24% of survey respondents do expect to see Limited Partnership interests change hands in their funds.

JUST OVER HALF OF VCs SEE FUNDRAISING TAKING LONGER THAN PREVIOUSLY ANTICIPATED

Most respondents expect their next fundraise to be delayed or prolonged, but a notable 39% believe fundraising will remain on schedule over the next 18 months or so.

SAMPLE SIZE AND METHODOLOGY: The Industry Ventures COVID-19 survey was designed to collect VC industry views on the coronavirus pandemic and its effects. The sample size was 117 VC firms.